Oct 29, 2019

Beyond Meat plunges as analysts cut price targets after earnings

, Bloomberg News

Beyond Meat shares drop after latest earnings

VIDEO SIGN OUT

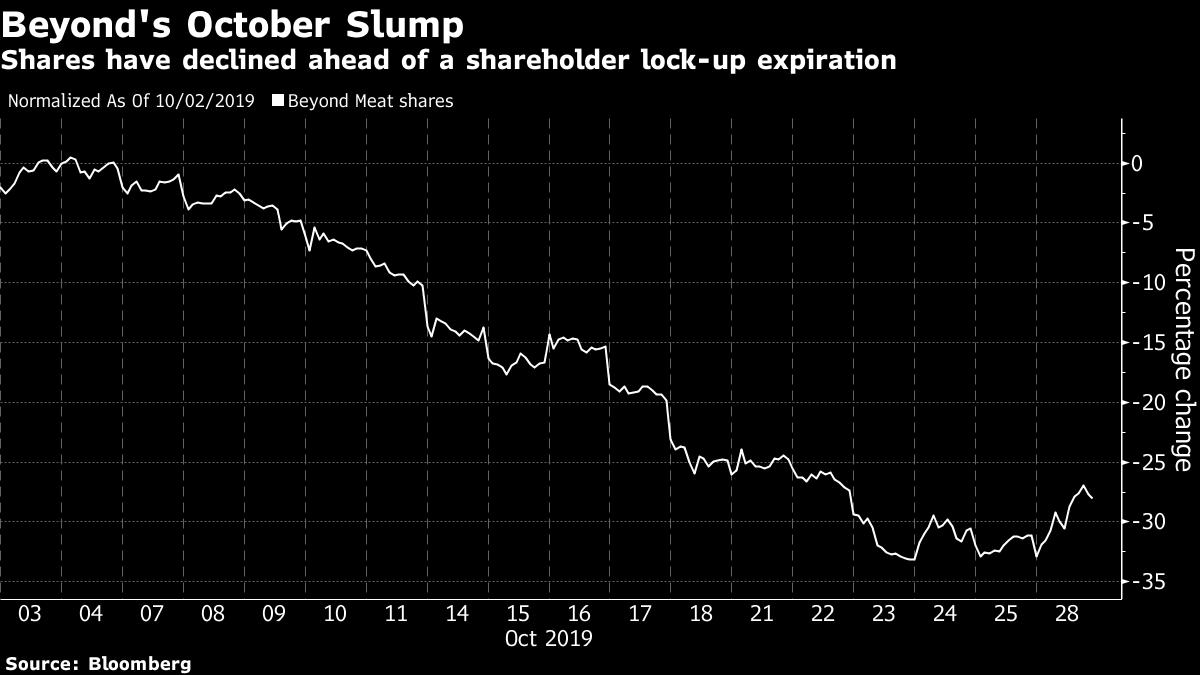

Beyond Meat Inc. lost more than a fifth of its value on Tuesday as analysts cut their price targets following results that raised questions about rising competition, slowing growth and higher operational costs. The stock’s lockup expiry also contributed to the weakness.

A boost to the company’s sales outlook might not be enough to impress investors with already elevated expectations for the plant-based burger maker, ahead of a likely increase in near-term competitive pressures, analysts said. The low-end of the revised forecast may also suggest fourth-quarter sales could slow from the third quarter pace, Jefferies analysts said.

Jefferies, Wells Fargo and JPMorgan were among banks that lowered price targets on the stock, according to Bloomberg data.

Results were also overshadowed by Tuesday’s expiration of insider-selling restrictions. Under the arrangement, about 75 per cent of shares outstanding become eligible for sale today, according to an Oct. 28 note from Sanford C. Bernstein. Beyond Meat was already down 29 per cent month-to-date ahead of the expiry.

Beyond Meat shares fell as much as 24 per cent to US$80 per share in intraday trading in New York Tuesday. The stock hasn’t traded that low since May 24. Shares have trimmed their post-IPO gains to 237 per cent.

Here’s a summary of analyst views following the earnings report:

Jefferies, Kevin Grundy

(Hold, PT cut to $115 from $190)

Quarterly results beat across the board, but while full-year guidance was raised, it may not be enough to clear the high bar set by the Street, particularly as competitive intensity ramps up and the end of a lockup weighs on the shares. Moreover, the low-end of updated 2019 guidance implies a sequential deceleration in the fourth quarter.

Even so, Beyond Meat is perhaps the best early stage growth story in staples with significant scope to expand penetration globally.

Wells Fargo, John Joseph Baumgartner

(Market perform, PT cut to US$100 from US$125)

With competitive entrants ramping up through the first half of fiscal 2020, expect Beyond Meat to increase its promotions. There’s also a need for higher operational expenditure to support domestic brand investment and to build up international capabilities.

Amid limited visibility and likely “competitive turbulence” in fiscal 2020, continue to recommend Danone SA and Nomad Foods Ltd. for exposure to long-term plant-based theme.

Quarterly net sales “easily” beat the Street, but a “rich” valuation already reflects high expectations.

Bloomberg Intelligence, Jennifer Bartashus

Revenue growth and a first quarterly profit is a positive step toward long-term sustainable earnings, but is excessively overshadowed by uncertainty around the effects of exiting its post-IPO lockup period.

While rapid international expansion could be a boon, it runs the risk of splitting focus during the company’s “still-nascent” growth. Gross margin could be affected by investments to help drive product prices closer to parity with meat counterparts, but can potentially be offset by cost-control initiatives.

Product traction points to a long-term opportunity versus a fad.

--With assistance from James Cone.